Cap Rate vs Cash-on-Cash: The Two Numbers Investors Mix Up

Cap rate measures the property; cash-on-cash measures your money. What each number can and can't tell you, and how sellers use the confusion.

Cap rate measures the property; cash-on-cash measures your money. Net operating income divided by price tells you what the asset earns with no financing in the picture. Annual cash flow divided by cash invested tells you what your dollars earn under your actual loan. Confusing the two — or letting a seller confuse them for you — is how mediocre deals get bought.

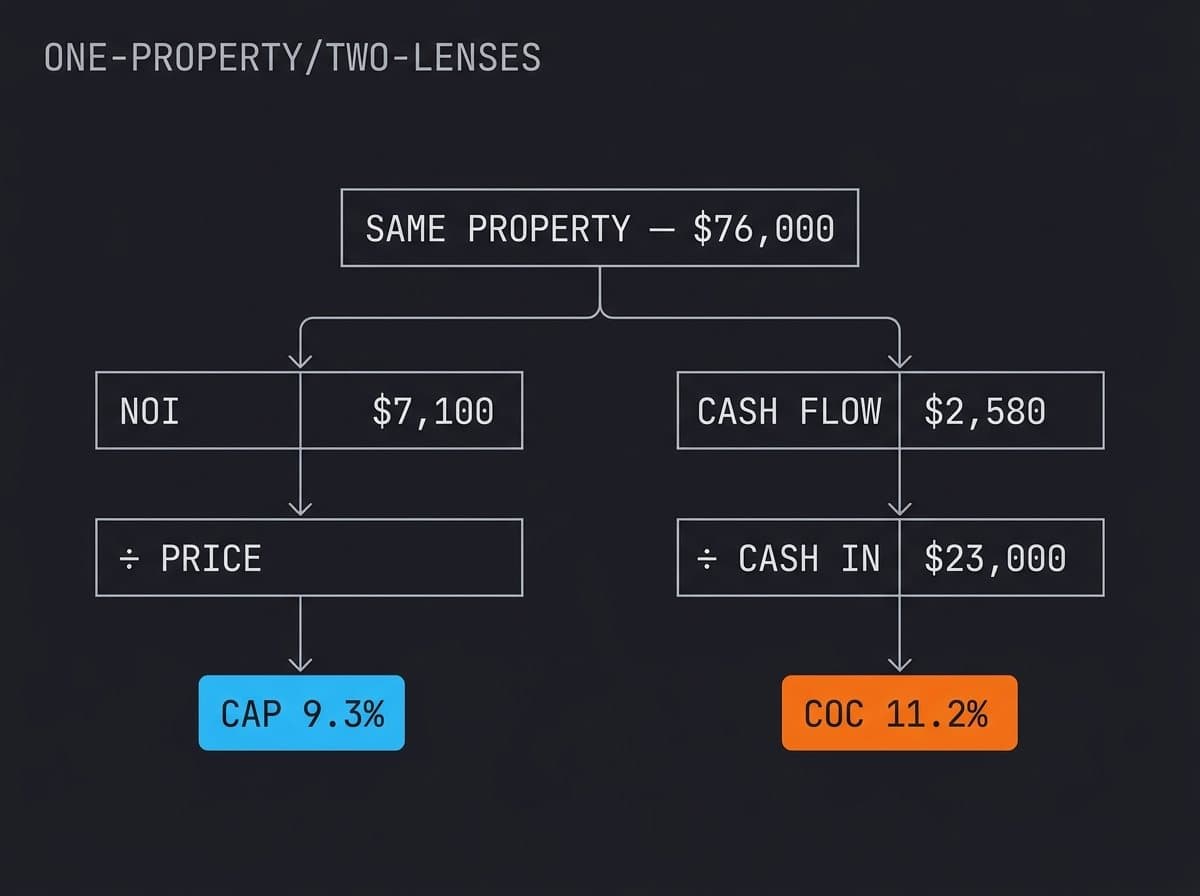

The two definitions, with the same house

Take a renovated river-town single-family at a $76,000 purchase, renting at $950 with honest expenses of $4,300 a year.

Representative deal — both lenses on one property

Cap rate (9.3%) is the unlevered yield: what the property produces relative to its full price, as if bought in cash. Because financing isn't in the formula, the number is the same for every buyer — which is exactly what makes it comparable across properties and across markets.

Cash-on-cash (11.2%) is the levered yield: after the mortgage payment, what's left relative to the cash you actually deployed. It changes with every financing structure — which is what makes it personal, and what makes it quotable into nonsense by anyone who picks a flattering loan scenario.

Why the confusion costs money

Sellers and promoters exploit the gap between the two numbers in predictable ways. A "12% return!" headline is usually a cash-on-cash figure built on maximum leverage and minimum expenses. An "8% cap" flyer often computes NOI from projected rents with management and capital reserves quietly missing.

The defense is mechanical, not clever: recompute both numbers from raw inputs — actual rent, every expense line, your real financing. The same skepticism you'd apply to a cost claim applies to a return claim, because a return claim is just a cost claim divided into a rent claim.

How to use each number

Use cap rate to compare and to sanity-check markets

Because it strips financing, cap rate puts a Keokuk single-family and a Phoenix condo on the same footing. When the 1% screen says a market is interesting, the cap rate on real expenses says whether it survives contact with operating reality.

Use cash-on-cash to judge your deployment

This is the number your capital experiences. Run it with your actual loan terms and a vacancy and maintenance reserve you believe. If it only clears your bar with 30-year-best financing assumptions, the deal is borrowing its quality from the spreadsheet.

Check the expense lines both share

Both formulas live or die on honest expenses. The lines most often missing from advertised numbers: management (even if self-managing — your time prices in eventually), vacancy, capital reserves, and the real tax bill. Add what's missing, recompute, and watch advertised returns shrink to their true size.

Know what neither number sees

Neither metric prices equity captured at purchase, neighborhood trajectory, or tenant-base durability. A 9% cap on a failing block and a 9% cap on a stable one are not the same investment — the number can't tell you that; the diligence does.

How Pando handles this

Pando deal pages publish the raw inputs — in-place or comparable rent, the full expense schedule, the transfer price — so both numbers can be computed by you rather than quoted at you. The evaluation behind every deal runs on real expenses by policy: management priced in, reserves priced in, the tax bill pulled from county records. A return metric you computed from our raw numbers is worth ten we could have advertised.

FAQ

Cap rate vs cash-on-cash — the short version? Cap rate: property's income ÷ price, no financing — describes the asset. Cash-on-cash: your cash flow ÷ your cash in — describes your position.

Which matters more? Cap rate to compare deals and markets; cash-on-cash to judge your own capital's deployment. Use both.

What's a good cap rate? Market-relative — small stable Midwest markets commonly evaluate at 8–10% on honest expenses. The honesty matters more than the number.

How are these numbers gamed? Projected rents, missing expense lines, flattering financing scenarios. Recompute from raw inputs, always.

Next step

See how Pando publishes deal numbers — or request access and run both metrics on a live transfer yourself.

See the discipline in practice.

Vetted investors get first look at every deal Pando announces — evaluation numbers, not marketing numbers.

The console has read this article. Ask for the short version, the main points, or anything it raised.