Wholesale vs Turnkey vs Syndication: Which Model Fits Which Investor

The three main ways to buy real estate at a distance — wholesale transfer, turnkey, and syndication — compared on control, fees, equity, and who each fits.

Wholesale transfer, turnkey, and syndication are the three serious ways to own income real estate at a distance — and they differ on exactly four axes: what you control, what you pay in fees, when your equity arrives, and whose risk you're carrying. Map yourself onto those axes and the right model picks itself.

The three models in one table

| Axis | Wholesale transfer | Turnkey | Syndication |

|---|---|---|---|

| What you own | The property, title in your name | The property, title in your name | LP shares in an entity |

| Price vs comp value | Below comp — equity at close | At comp (retail) | N/A — you own a pro rata slice |

| Fee transparency | Spread visible against comps | Margin embedded in price | Acquisition + AUM + promote layers |

| Control | Full | Full | None — sponsor decides |

| Liquidity | Sell when you choose (slower markets) | Sell when you choose | Locked until sponsor exits |

| Your job | Verify, then own | Verify harder, then own | Vet the sponsor |

| Income starts | At tenant placement | Often day one (tenant in place) | At first distribution |

The table is the summary. The texture is below.

Wholesale transfer: buy the discount

A wholesale operator acquires distressed property below replacement cost, renovates it, and assigns or transfers it to you below its post-renovation comparable value. The operator's margin was created when they bought right — not by charging you retail — so the discount survives into your basis as equity at close.

The strength: you own the asset outright with a margin of safety that exists at closing, not in a projection.

The honest weakness: the model's reputation. The barrier to calling yourself a wholesaler is low, so verification is your job — control, value, paperwork — every time.

Fits: investors who want direct ownership and verifiable day-one value, and who will actually do the verification.

Turnkey: buy the convenience

A turnkey provider sells a renovated, often tenant-occupied rental at full market price, frequently with in-house management attached. The product is convenience: close, collect rent, done.

The strength: genuinely low friction, income from day one.

The honest weakness: you paid retail. Every dollar of the provider's acquisition discount and renovation margin stayed with the provider; your return now depends entirely on the rent holding and the market growing. If the pro forma needed optimistic rent growth to pencil, you bought a projection at full price. The in-house management also bundles your biggest ongoing relationship with the party that just sold to you — read those incentives carefully.

Fits: investors who consciously value convenience over basis and verify the rent roll hard.

Syndication: buy the sponsor

In a syndication you wire capital into an entity that buys a larger asset — an apartment complex, a portfolio — and a sponsor runs everything. You receive distributions and a K-1; the sponsor receives fees at acquisition, fees during the hold, and a promote at exit.

The strength: true passivity and access to asset classes you can't buy alone.

The honest weakness: you've traded every control for trust in one party. Capital calls arrive whether convenient or not; reporting is whatever the sponsor provides; the exit happens on their timeline; and the fee stack — often 1–2% acquisition, ongoing asset management, plus 20–30% of profits above a hurdle — compounds quietly across the hold. You aren't really buying the building. You're buying the sponsor's judgment and incentives.

Fits: investors with capital they genuinely never want to think about, who can evaluate a sponsor as rigorously as a property.

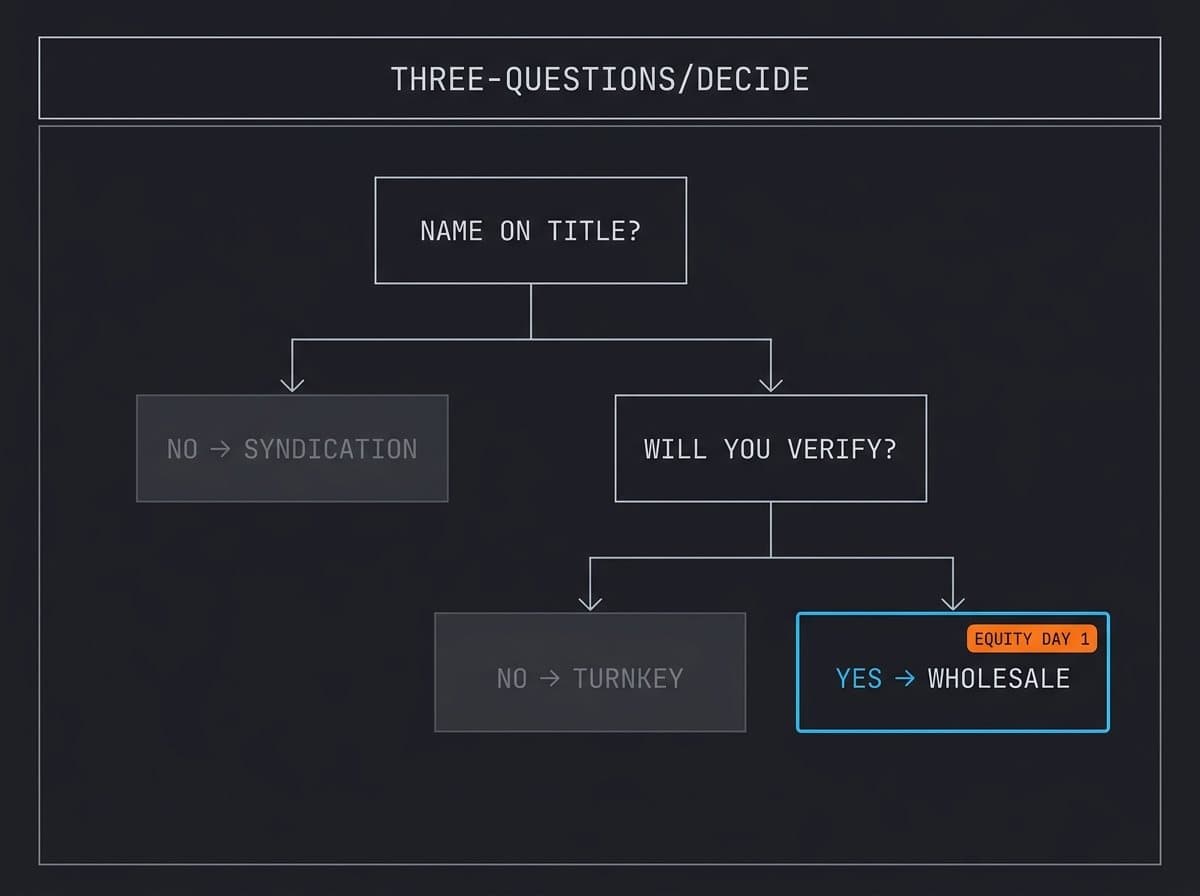

The decision in three questions

- Do you want your name on title? No → syndication is the only model that fits. Yes → continue.

- Will you verify a deal yourself — comps, appraisal, paperwork? No → pay the turnkey premium consciously. Yes → continue.

- Where do you want the operator's margin? Built into your retail price (turnkey) or earned at acquisition with the discount passed through (wholesale transfer)? That's the whole difference.

How Pando handles this

Pando runs the wholesale-transfer model with the verification problem treated as the product: every deal page publishes the evaluation numbers, every property clears eleven buy-box criteria before an investor sees it, disclosure runs under Iowa's HF 2374 framework, and the transfer price sits below renovated comp value so the equity lands on your side. No pooled fund, no capital calls, no promote — you own the property, and the spread we earned is visible math, not embedded margin.

FAQ

What's the difference between turnkey and wholesale? Same renovated product, opposite pricing logic: turnkey sells at comp value; wholesale transfers below it, so the discount becomes your equity.

Is syndication better than direct ownership? It's more passive and more diversified — and you trade away control, liquidity, and fee transparency to get that. Neither is "better"; they're different jobs.

Which model has the lowest fees? Wholesale transfer is the most transparent — the spread is visible against comps. Syndication stacks the most layers.

Can I lose money in each? Yes. The question is where the risk lives: the asset (wholesale), the retail price (turnkey), or the sponsor (syndication).

Next step

If direct ownership with verifiable day-one equity is your lane, request access and put a live Pando deal through your own diligence.

See the discipline in practice.

Vetted investors get first look at every deal Pando announces — evaluation numbers, not marketing numbers.

The console has read this article. Ask for the short version, the main points, or anything it raised.