Equity at Close, Explained: The Math of Buying Below Comp Value

Instant equity is the gap between what you pay and what the property appraises for on day one. Here's the math, the catch to check for, and how to verify it.

Instant equity is the difference between what you pay for a property and what it appraises for on the day you take title. It is not a projection or a pro forma — if the comparable-sales work behind it is honest, it exists at the closing table and you can verify it with your own appraisal before wiring a dollar.

What "equity at close" actually is

Most real-estate value claims live in the future: projected rents, projected appreciation, projected exit prices. Equity at close lives in the present tense.

The mechanic is simple. A disciplined operator acquires a distressed property below replacement cost, renovates it to a rent-ready standard, and transfers it to an investor at a price below the post-renovation comparable value. The gap between your transfer price and that comp value is your equity — on day one, not in year five.

Here's the shape of the math on a representative Midwest river-town deal:

| Line | Amount |

|---|---|

| Acquisition (distressed) | $42,000 |

| Renovation | $24,000 |

| Transfer price to investor | $76,000 |

| Post-renovation comp value | $95,000 |

| Equity at close | $19,000 (20%) |

The investor pays $76,000 and owns a property that appraises at $95,000. The operator's margin lives inside the spread between total cost basis and transfer price. Both parties are paid by the same discipline: buying right at the front of the deal.

Why it matters

If you've evaluated turnkey providers, you've seen the opposite pattern: retail price, fresh paint, and a pro forma that needs three years of rent growth to justify the number you paid. You carried all the market risk; the seller captured all the margin.

Equity at close inverts that. The discount is captured for you at acquisition, survives the renovation budget, and lands on your side of the closing statement. The market can go sideways for two years and your position still started ahead instead of underwater.

It also changes what diligence means. Instead of auditing someone's rent-growth assumptions, you're auditing one number — the comp value — and that's a number you can check independently.

How to run the math yourself

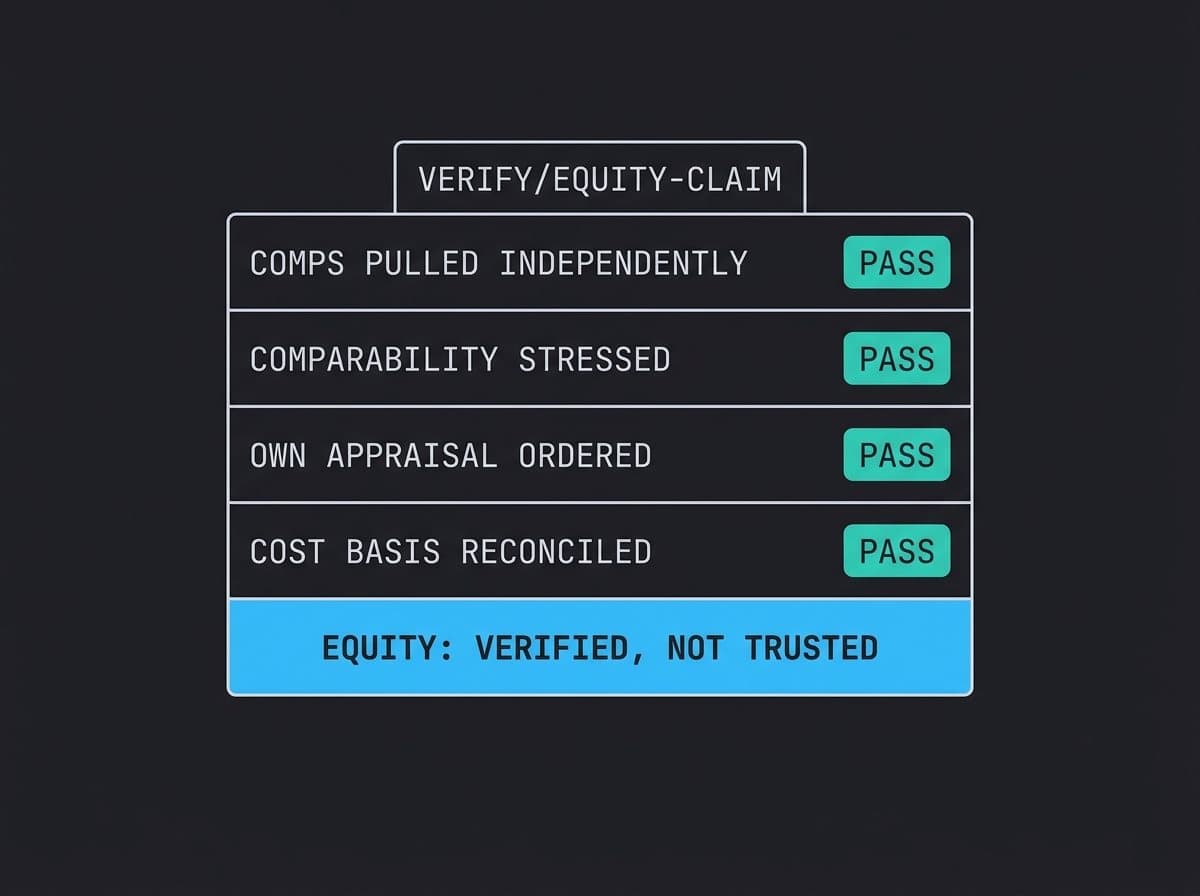

Treat every "instant equity" claim as a hypothesis to test. Four steps:

1. Pull the comps yourself

Don't accept the seller's comp sheet as the final word. Pull recent sales in the same market — same town, not a better one nearby — and filter to properties in post-renovation condition. Three to five genuinely comparable sales beat ten loose ones. (This is one item on the full wholesaler-verification checklist — worth running end to end.)

2. Stress the comparability

The most common way an equity claim falls apart: the comps are real but not comparable. A sale from the historic district doesn't comp a property by the rail line. A sale from a hot quarter eighteen months ago doesn't comp today. If the equity only exists with the most generous comps, price it as if it doesn't.

3. Order your own appraisal

This is the step that separates verifiable equity from marketing. A few hundred dollars buys an independent opinion of value before closing. An operator confident in their number will never discourage this — treat any resistance as your answer.

4. Check the basis, not just the gap

Ask what the operator paid and what the renovation actually cost. You don't need their margin to be small — you need the total story to reconcile. Equity that exists because the operator bought well is durable. "Equity" that exists because the comp value is inflated evaporates at your refinance appraisal.

How Pando handles this

Every Pando deal page shows the same numbers our own evaluation used — acquisition logic, renovation scope, transfer price, and the comparable-sales basis for the value. Properties only reach investors after clearing all eleven buy-box criteria, and the average across closed deals has run high-teens equity at close.

We set the transfer price below comp value on purpose. The model is velocity: a fair spread on each deal, repeated, beats squeezing the last dollar out of any single one — how that compares to turnkey and syndication is its own article. That's also why the math is published instead of summarized — a skeptical investor who checks our comps and finds them honest is worth more to us than ten who took the brochure's word.

FAQ

What does instant equity mean in real estate? The difference between your purchase price and the property's appraised value on the day you close. Pay $76,000 for a property that appraises at $95,000 and you closed with $19,000 — about 20% — of equity without waiting for the market.

Is instant equity at close guaranteed? No claim in real estate should use that word. It's verifiable, which is better: order your own appraisal before you wire anything.

If the deal is so good, why doesn't the operator keep it? Velocity. A wholesale operator earns a spread on each transfer and recycles capital into the next acquisition. Holding everything would cap the pipeline at whatever they could finance.

How do I verify equity at close before buying? Pull the comps yourself, stress their comparability, order an independent appraisal, and make sure the operator's total cost basis reconciles with the value story.

Next step

See how the full process works from sourcing through transfer — or request access and check the math on a live deal yourself.

See the discipline in practice.

Vetted investors get first look at every deal Pando announces — evaluation numbers, not marketing numbers.

The console has read this article. Ask for the short version, the main points, or anything it raised.