Insuring an Older Rental: ACV, RCV, and the Clauses That Bite

Insuring a 1920s rental isn't like insuring your house. ACV vs RCV, vacancy clauses, knob-and-tube exclusions — what to buy and what to watch.

Insuring a 1920s rental is its own discipline: you need a landlord dwelling-fire policy, not a homeowner's form; replacement-cost valuation, not depreciated payouts; and clean answers on the three things carriers fear in old stock — wiring, roofs, and vacancy. Priced right, the line is modest. Assumed casually, it's where one bad night erases the year.

The form: landlord, not homeowner

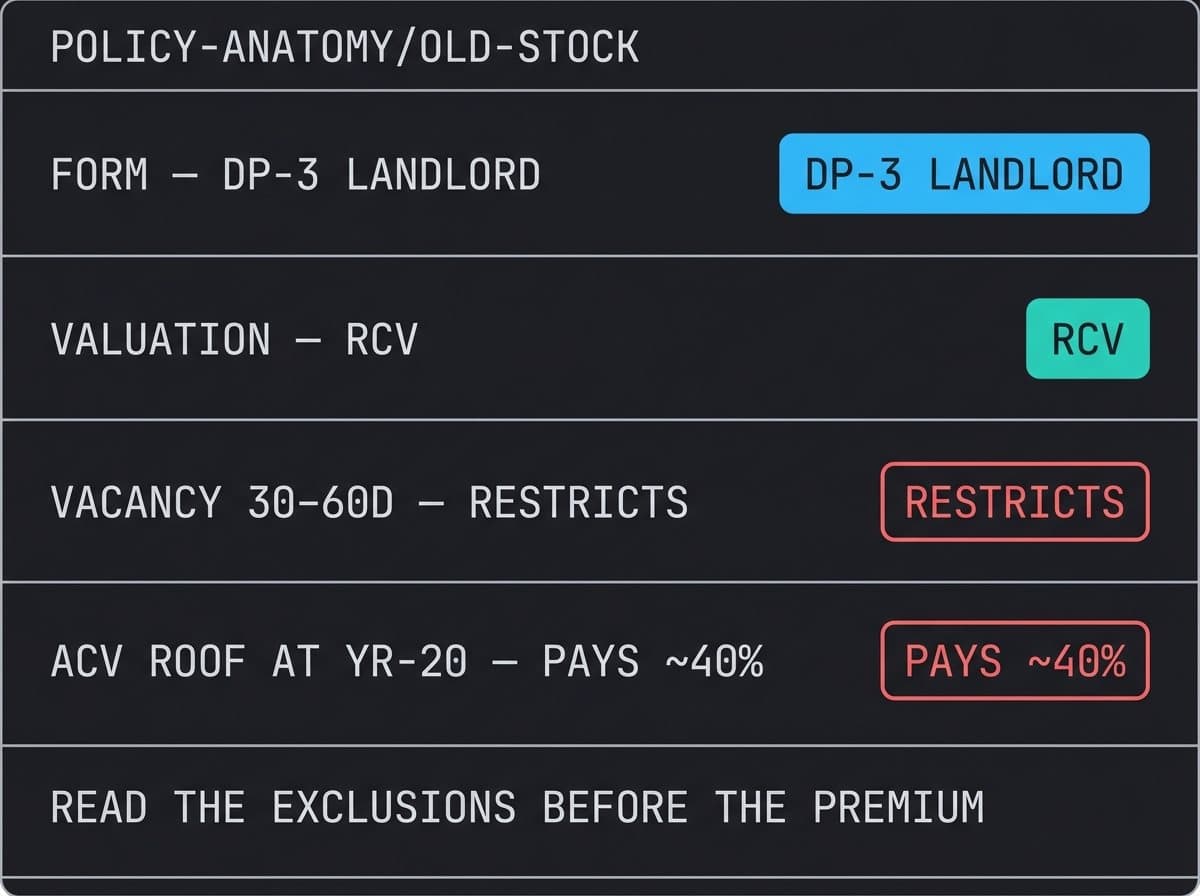

A rental needs a dwelling-fire policy (the DP series). A homeowner's form on a tenant-occupied property risks denied claims for misrepresented occupancy — the cheapest way to discover you were never covered. Within the DP series: DP-1 is bare-bones named-perils at ACV; DP-3 is open-perils and supports replacement cost. On renovated stock, the DP-3 premium difference is usually small against what it changes at claim time. Add liability ($500K+, with your entity structure named correctly) and loss-of-rents, which pays the rent while a covered loss is repaired.

The valuation decision: ACV vs RCV

This is the clause that decides whether old-house insurance works.

A $12,000 roof at year 20 of a 25-year life might settle near $3,000–$5,000 under actual-cash-value — the depreciated worth, not the repair bill. Replacement-cost valuation exists to close exactly this gap.

Carriers may resist full RCV on very old structures, or price dwelling value off rebuild cost that far exceeds market price — a $85,000 river-town house can carry a $220,000 rebuild number. That gap is normal; insure to rebuild reality, not purchase price, or accept a stated-value form with eyes open. What you don't do is let the agent quote the cheapest ACV form and call it equivalent.

The clauses that bite in old stock

Wiring and systems questions — answer with receipts

Applications ask about knob-and-tube, fuse panels, galvanized plumbing, roof age. Misstating them is claim-denial bait; the documented century-house renovation is the answer that fixes both premium and insurability. A rewire receipt is an insurance asset.

Vacancy restrictions — the 30/60-day trap

Vacant 30–60 days and key coverages quietly shut off. Between tenants on a renovation or a slow placement, buy the vacancy endorsement. The week you skip is the week the pipe lets go.

Water exclusions — read them twice

Sudden-and-accidental water is covered; seepage, sewer backup, and sump failure usually aren't without endorsements. On houses with century-old laterals, the sewer-backup endorsement is cheap relative to what it covers.

Roof schedules — the new fine print

Carriers increasingly apply roof payment schedules that step coverage down by age regardless of form. Ask directly: "how does this policy pay a 15-year-old roof?" The answer sorts carriers fast.

Pricing it into the deal

Get a real quote during diligence, not after closing — occupancy, wiring answers, and roof age move premiums enough to matter at river-town price points. A representative renovated Midwest single-family runs modest hundreds per year, not the storm-state multiples — one of the quieter lines in the regional comparison — but only the bound quote counts. Then put the premium in the expense stack you compute returns from, where it belongs.

How Pando handles this

The renovation documentation that transfers with every Pando deal — rewire receipts, roof dates, plumbing updates, scoped laterals — is also your insurance application, answered with evidence. Deals carry the system ledger insurers actually ask about, which is why renovated transfers quote clean while as-is stock quotes ugly. Our expense modeling uses a quoted premium, not a guess, and the deal page shows the number so your cash-flow math starts from reality.

FAQ

What policy form do I need? Landlord dwelling-fire (DP-3 preferred on renovated stock) with liability and loss-of-rents — never a homeowner's form on a rental.

ACV vs RCV in one line? RCV pays the repair bill; ACV pays the repair bill minus age. On old houses, age is most of the bill.

The vacancy trap? Coverage restricts after 30–60 empty days — endorse it during any gap.

Biggest old-house insurability fix? A documented rewire. It moves premium, coverage, and carrier appetite all at once.

Next step

See how system documentation travels with a Pando deal — or request access and hand a live deal's ledger to your insurance agent for a real quote.

See the discipline in practice.

Vetted investors get first look at every deal Pando announces — evaluation numbers, not marketing numbers.

The console has read this article. Ask for the short version, the main points, or anything it raised.